(1) Tourism Industry is very much positive. From my market survey and study on this industry, I understand that there are many foreigners travelling to Malaysia via air, sea or land. Beneficial to ---- > CLMT, Parkson, SATS, soon Hospitality and Leisure industry, Tunepro, Airport, Marine or Sea-related Industries ! LOOK! I have CRUISES Schedule to prove that Tourism Industry is BACK! BOOMING SOON! PENANG PORT will be getting benefit very much! 我亲自做场地考察,本身去经验港口的大邮轮,旅游业复苏了啊 (2) BAT not yet die but heading to face more CHALLENGE due to Shrinking Market Size --- heading toward Sunset - I used to invest in BAT long time ago but ever since GEG proposed by Goverment I mark BAT under WATCH LIST which is a risky investment - Start to conduct market survey and analysis on several things related to Health Awareness and Nicotine Addiction - Noted more and more GYM, Health Related Activities and Health Products are launched and gain market favour ----- > indication of p...

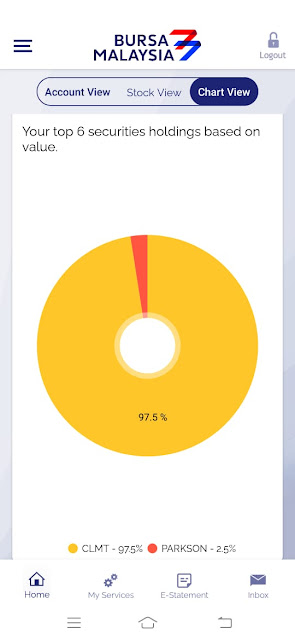

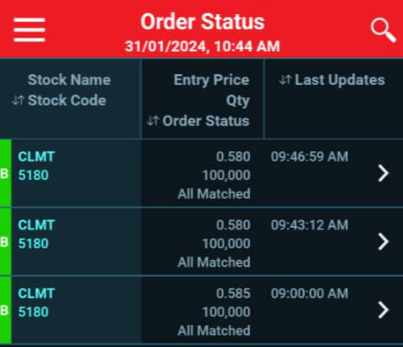

我也不需要说太多,大家看看我一直提倡的几个股票,就有答案。 Bursa ---- CLMT - recovery is under progress. More and more enhancement of assets will be achieved due to master plan in Penang (Industrialisation, Transportation and etc) - opening of Gurney Bay opposite Gurney Plaza - disposal of non-performing assets such as 3 Damansara - Glenmarie Shah Alam warehouse rental - soon to happen more and more REIT diversification - add more and add more, 80 cents to 1 ringgit is not an issue LOOK! Follower trusts me and add more and more Follower's result is not bad after 6-month Patience SGX ---- SATS - acquisition of Worldwide Flight Services adds more business presence globally - strong support from solid Temasek (Singapore Government) - monopoly in Changi Airport such that 60% or more is done by SATS - construction of Changi T5 is going to be commenced from 2025 which will be another catalyst - recovery of Tourism industry Bursa ---- AFFIN - the increase of stake by Sarawak is within expectation - 100% ...

If you are thinking that performance of PHB is bad in Q2 FY2023, I guess that you have not looked into details and analyse performance fairly by removing (1) Special Item; (2) Abnormal or Exceptional Item; (3) Non-Recurring Items; (4) Non-Cash items You will be impressed that based on analysis, Normalised Operating Profit Margin Normalised PBT Margin Normalised PAT Margin Normalised EBITDA for 30 June 2023 are EXCEPTIONALLY GOOD and IMPRESSIVE Even if you are not convinced with the above, you may refer to Segmental Performace Review, you will be impressed that PHB was doing very well Retail Revenue in totality is slightly lower than Q1 FY2023 but Retail Profit for Malaysia and China shows improvement. Significant Improvement in CHINA! As I have no time to analyse in detail every single ratio or numbers, I had decided to analyse only significant indicators which are more than sufficient for investors to gauge understanding at a glimpse! I always believe th...

Comments

Post a Comment